Understanding the fundamentals of commodity businesses can at times be quite an intriguing and a complex task - the erratic and cyclical nature of free market pricing lends itself to volatile earnings for commodity producing companies and in turn depressed returns on capital - a strict avoid for many factions of investors.

To invest meaningfully into a commoditized business requires a stringent due diligence of the factors that influence prices of the product manufactured - and this is an arduous process with a new landmine planted within every new metal bulletin that the prospective investor tries to make sense off!

To put it in the words of famed investor Basant Maheshwari -

"Analysts and Investors who try to predict metal prices should actually be on the London Metal exchange trading those very commodities."

However, the quest for generating Alpha often leads the wandering investor to uncharted territory - and that's exactly how I stumbled up on this particular business I'm going to try to make head and tail of. Take it as a narrative on a set of qualitative factors that are currently going right and wrong for the business.

When the DCM group was split up in 1990, Ajay, Vikram and Ajit Shriram were handed a near sick textile mill and the Kota chemical complex which was making a small annual profit - though they didn't know what it exactly made. That day marked the inception of DCM Shriram, one of the many off-shoots of DCM.

First, lets understand the business structure. DCM Shriram is an Indian conglomerate which operates in a variety of business - right from sugar to fertilizer to Chlorine. It has two chemical complexes - one in Bharuch and the other in Kota that are into manufactuing of Chlor-Alkalis(Caustic Soda and Chlorine) and PVC resins. The Kota complex also has a 3,80,000TPA Urea Plant. Besides, the company also has 3 sugar Mills in the UP with a combined capacity of 33,000TCD. The waste generated in the Kota plant is used as feedstock in the Cement plant which has a capacity of 4 lakh tonnes/annum. This plant was set up with technical assistance from Lafarge.

In addition to the Urea plant, the company is also involved in the trading of other agri-inputs like Insecticides and Pesticides. It also had brought a majority stake in seed provider 'Bioseed' which was later absorbed by the parent.

Finally, in an attempt to move up the value chain, the company forward integrated its PVC business and set up Fenesta - a new range of UPVC Windows. It also entered into a JV for Polymer compounding with Axiall LLC of the United States

As you go through the business structure, you'd realize that almost everything that the company does is subject to the vagaries of the commodity cycle - the prime culprits being the sugar and fertilizer division. There is very little that the company offers for the secular growth investor who is perennially on the hunt for brands that compound at super-normal rates without needing a single penny of incremental capital.

In fact since the turn of the decade DCMS has consistently faced strong headwinds in its operations . High power costs in the Chlor-Alkali business, sugar prices spiraling lower and the erratic nature of monsoons in the country have all contributed to a fairly turbulent time for the conglomerate. The icing though has been the failure of the Hariyali Kisan Bazaar(a series of rural retail outlets) which has been a constant cash burner for the better part of its existence. At it's peak in 2011-12, the venture contributed in excess of 15% to revenues and incurred yearly EBIT losses of nearly 100 crores

The spate of losses meant that the company had to carry out a significant downsizing of operations post FY'12, which led to a one time loss of ~55cr in FY'13. Consequently, the share of capital employed in Hariyali Kisaan Bazaar came from 14% in 2010 to 7% in 2013.

This in turn propelled return on capital employed of the consolidated entity jumping from 5.79% in 2012 to 13% in 2013. Gradual downsizing of the entity year after year meant that by the end of FY'15, Hariyali Kisan Bazaar didnt have any continuing operations.

Besides the problems of the HKB on one hand the sugar and fertilizer division continued to drag the business to lower nadirs with each passing day

Among-st all this chaos, burgeoning channel inventory in the international operations of Bioseeds meant another vertical that would need a restructuring exercise

Within this gloom and doom, the chemicals division did all the heavy lifting in terms of consolidated performance - both the Chlor-Alkalis and PVC Division delivered largely stable numbers albeit without any significant growth.

The very fundamentals of a cyclical business dictate that every bust is followed by euphoria and every euphoria is succeeded by despair. The last 2 years have witnessed a maverick turnaround in business operations which has resulted in the bottom-line more than doubling from 228cr in FY'15 to 550cr in FY'17 even as top-line hasn't moved the needle. All of this has culminated in the stock price moving up 3x from the lows of 113 in Feb 2016 to the recent historic highs of 410.

Before I delve deeper into the triggers that lie ahead for the business, let me take a microscopic view on what's changing for each division of the company.

Let's first understand the dynamics of the two biggest culprits

To begin with Fertilizers it is worth noting that India consumes 167kg of Urea/hectare, second only to Germany which consumes 230kg/hectare. Urea as a fertilizer is high in nitrogenous content and is readily available, hence becoming the preferred choice for the Indian Farmer. India consumes nearly 30million tonnes of Urea a year whereas domestic production is only in the range of 22-24 million tonnes. The demand-supply imbalance can be broadly attributed to the change in stance of the UPA Government towards Urea manufacturing and import when it came to power in 2004 (which eventually led to the emergence of Indian Potash Limited).

The un-viable NPS-3 Pricing formula which determined subsidy on the basis of a fixed retail price and ever increasing input costs led to the creation of a vicious circle by way of which Urea plants fell into a quagmire of ever widening losses. Besides, the diversion of Urea for industrial use in items such as plywood and even staples such as milk led to a massive backlog of subsidies for producers. All of these issues culminated in a traumatizing first half of the decade for all fertilizer companies with some of them folding up en route the tumultuous journey. DCM Shriram was no exception - the numbers discussed in the preceding paras reek of immense stress.

The end to this came with the implementation of the Urea Policy of 2015 wherein the new government at the helm pioneered a slew of reforms such as mandating all of the Urea produced in the country to be neem coated so as to prevent its diversion to industry, the gas pooling mechanism by way which all plants would now get feed stock at uniform prices and higher incentives for production above a specified level(which needless to say, was UN-remunerative earlier) . Coupled with this, crashing gas prices and clearance of past subsidy dues through the special banking arrangement have gone a long way in healing balance sheets and adding much needed green to the Profit and Loss statements.

Again, our company hasn't been an exception

Since its coming to power, the NDA government has sworn to quicken the pace of subsidy clearances and reduce arrears through a special banking arrangement given to all fertilizer companies. With the implementation of the Urea Policy of 2015, companies have found it remunerative to produce at levels above reassessed capacity and this is exactly what the above graphic depicts. Pre 2015, even though the Kota plant operated at capacity levels north of 100% , increasing subsidy burden meant incremental capital burn with each passing year. This coupled with the non-remunerative and 'impractical' NPS-3 pricing formulae meant that Return on capital slid from the dizzy heights of 50% to low single digits by 2014. ( Side note : re-assessed capacity for DCMS stands at 379,000 TPA)

Post the implementation of the Urea Policy of 2015 which re-established the viability of excess production coupled with faster subsidy outgoes (subsidy outstanding at the end of FY'17 for the company has been pegged at 347cr v/ 451cr a year earlier) the business as a whole has become relatively less capital intensive and far more rewarding. This is evident from the near doubling of RocE's from 2014 to the end of FY'17 even though quantity sold has fallen.

Future Outlook - This space now looks much attractive as it hopes to get a series of fresh investments after a drought of 15 years as the central government plans to revive three sick fertilizer units and the possible entry of Jindal Steel into the sector. The implementation of the direct benefit transfer has hit a temporary snag but there seems to be a new found mojo among incumbents that the future will be relatively brighter than the rather inglorious past. With monsoons predicted to be at 98% of Long period average, there seems to be some head of steam building up at last.

The sugar cycle is fraught with its own share of dizzying uncertainty and timing it to perfection is a skill that resides in a select few. After ending the year in a surplus for six straight years between 2010 and 2016, global sugar stocks finally moved into deficit as India turned net importer of the commodity due to severe drought in the state of Maharashtra(home to 40% of the country's sugar production.) This coupled with the continuous diversion of sugarcane towards ethanol production in Brazil meant that there was a significant supply shortage which took prices on the ICE from lows of 10.5cents/lb in mid 2015 to recent highs of 22.5cents/lb.

The Indian sugar industry has long been at the mercy of both the central and state governments who have used the commodity as a popular means of populism among the rural population of the country. Sugar companies have perennially complained about the 'step-son' like treatment given to them at the behest of vote bank politics and the goverment's mandate of 'welfare of the poor.' Fixing of cane prices both at the central and state government levels dosent take into consideration the price of the final product - Sugar, as a result of which sugar mills, like fertilizer companies have been at the forefront of value destruction in the industry. The Rangarajan committee of 2014 alleviated a significant burden off the companies though there remains a lot more that needs to be done to completely take the shackles off the sector

DCM Shriram owns three sugar mills with a combined capacity of 33,000TCD and a co-generation facility which generates 94mw of power annually out of which 51mw is sold in the market. After reporting a De-growth in volumes of cane crushed between 2010-2016(2013 being an exception), FY'17 proved to be the turning year for the division volumes of cane crushed in the crushing season jumped from 282000MT in fy'16 to 412000 with an average recovery of ~11.1% . This led to sugar volumes jumping from 28.2 lac quintals in fy'16(with an average realization of 2638/quintal) to 36.6 lac quintals in fy'17(with an average realization of ~3530/quintal.)

Future Outlook - Sugar prices on ICE have nearly halved from the heights of 22.5cents/lb to settle in a range between 12.5-13 cents/lb currently. This hasn't had much of a ripple in domestic realizations though as top managements expect prices to remain stable. Tamil Nadu has witnessed its most severe drought in the past 100 years which means output from the 4th largest sugar producer from the country is likely to be tepid. On the other hand, Maharashtra is expected to bounce back with a 74'% increase in sugar production in the ensuing crushing season. International prices could stabilize around these levels going ahead as 13cents/lb is deemed to be the price at which more and more mills in Brazil divert their cane towards production of Ethanol. Another factor that could lend support to prices going ahead is that the US Department of Agriculture expects imports into India to increase in the coming year in-spite of higher production

Hence on the backdrop of largely stable prices, the sugar division is poised to witness another year of higher cane production prima facie due to higher cane acreage in the 2016 planting season. With another year of normal monsoon on the anvil, sugar production for the company could be set to touch newer highs in coming times.

Capital allocation remains the primary criterion when we judge management attitude towards the minority shareholder. DCM's management scores a high grade in this regard. Quick to smell the cash burn in the HKB Venture, the management has also reacted to the burgeoning working capital needs in the farm solutions business by downsizing its trading of complex fertilizers.

This is what the management had to say in the conference call for Q4 fy'17 -

The farm solutions division remains a trading business by and large and any further scaling down on operations would only lead to increased delta in operating margins on the whole.

The chemicals business remains the bell-weather for the company by far. Within this division the company has a 1280TPD capacity(recently expanded from 780 tpd) of Chlor-Alkalis which it manufactures in the ratio of 1:0.88(meaning that for every 1mt of Caustic Soda manufactured, it gets 0.88tonnes of chlorine.) The Chlorine so obtained is then partly sold in open market and partly used in the manufacturing of PVC Resins. The PVC division is further integrated into polymer compounding and the Fenesta brand - which makes PVC frames for windows

Let me touch upon each product specifically -

Future Outlook - The capital employed in this segment has more than doubled in the last 3 years due to the recent capacity expansion at Bharuch and the planned expansion at Kota for the coming year. As a result, RoCE's have halved - as the new capacities come on stream and get fully absorbed. Management expects the recently upgraded Bharuch to contribute meaningfully for the full year thereby propelling capital efficiency and in turn driving RoCE's. (side note - current capacity utilization stands at 77% , management expects this to cross 80 comfortably in the future. The management has upgraded the Bharuch facility with the membrane cell technology which further aids power efficiency. It plans to do the same in the Kota plant in the coming year)

The Indian PVC Resin market stands currently at around 3-3.5 Million tonnes/annum. At current prices of 75-77/kg the industry size is pegged in the region of 22,500 to 25,000 crores. DCMS has a 70,000 tonne capacity and runs at utilization north of 90% . With no capex planned as of now this unit becomes the cash cow within the chemical division as the working capital cycle in this business is miniscule which helps management to generate sufficient free cash to fund its overall operations

Among the smaller businesses, Bioseeds has been a volatile business for the company courtesy the overseas operations in Philipines and Vietnam and price regulations on Bt cotton seeds domestically. DCMS has taken a one time hit of 85cr in Bioseed's international operations owing to 'high gestation periods and large losses.' The domestic operations are set to pick up steam as farmers shift from sowing pulses(due to their UN-remunerative MSP's) to cotton.

Any analysis isn't complete without a hygiene check of the books. We examined all the available subsidiaries of DCMS and found a couple of striking points

DCM Shriram Infrastructure is a step down subsidiary of DCM Shriram Investments and Finance which in turn is a subsidiary of DCMS(the parent.) What we found was that DCMS has invested a sum of 30cr approx in this entity through an inter-corporate deposit. This money has been invested in some sort of fixed asset addition which seems to be stuck in the CWIP phase. As per available data between 2014 and 2016, this has remained status quo without any further information since.

Another noteworthy point is a 95cr loan in Shriram Bioseed ventures given by the parent. This presumably forms part of the 85cr hit that DCMS standalone has taken on its books this year as impairment in the overseas operations of Bioseed

'

This in turn propelled return on capital employed of the consolidated entity jumping from 5.79% in 2012 to 13% in 2013. Gradual downsizing of the entity year after year meant that by the end of FY'15, Hariyali Kisan Bazaar didnt have any continuing operations.

Besides the problems of the HKB on one hand the sugar and fertilizer division continued to drag the business to lower nadirs with each passing day

| |

| (Looking at data till FY'15, margins of the combined business fell from 7 % in FY'10 to a negative 1% in FY'15. Hence, a significant portion of value got destroyed in the three businesses discussed.) |

Among-st all this chaos, burgeoning channel inventory in the international operations of Bioseeds meant another vertical that would need a restructuring exercise

| |

| A snippet from the 2014 Annual Report |

Within this gloom and doom, the chemicals division did all the heavy lifting in terms of consolidated performance - both the Chlor-Alkalis and PVC Division delivered largely stable numbers albeit without any significant growth.

The very fundamentals of a cyclical business dictate that every bust is followed by euphoria and every euphoria is succeeded by despair. The last 2 years have witnessed a maverick turnaround in business operations which has resulted in the bottom-line more than doubling from 228cr in FY'15 to 550cr in FY'17 even as top-line hasn't moved the needle. All of this has culminated in the stock price moving up 3x from the lows of 113 in Feb 2016 to the recent historic highs of 410.

Before I delve deeper into the triggers that lie ahead for the business, let me take a microscopic view on what's changing for each division of the company.

Let's first understand the dynamics of the two biggest culprits

To begin with Fertilizers it is worth noting that India consumes 167kg of Urea/hectare, second only to Germany which consumes 230kg/hectare. Urea as a fertilizer is high in nitrogenous content and is readily available, hence becoming the preferred choice for the Indian Farmer. India consumes nearly 30million tonnes of Urea a year whereas domestic production is only in the range of 22-24 million tonnes. The demand-supply imbalance can be broadly attributed to the change in stance of the UPA Government towards Urea manufacturing and import when it came to power in 2004 (which eventually led to the emergence of Indian Potash Limited).

The un-viable NPS-3 Pricing formula which determined subsidy on the basis of a fixed retail price and ever increasing input costs led to the creation of a vicious circle by way of which Urea plants fell into a quagmire of ever widening losses. Besides, the diversion of Urea for industrial use in items such as plywood and even staples such as milk led to a massive backlog of subsidies for producers. All of these issues culminated in a traumatizing first half of the decade for all fertilizer companies with some of them folding up en route the tumultuous journey. DCM Shriram was no exception - the numbers discussed in the preceding paras reek of immense stress.

The end to this came with the implementation of the Urea Policy of 2015 wherein the new government at the helm pioneered a slew of reforms such as mandating all of the Urea produced in the country to be neem coated so as to prevent its diversion to industry, the gas pooling mechanism by way which all plants would now get feed stock at uniform prices and higher incentives for production above a specified level(which needless to say, was UN-remunerative earlier) . Coupled with this, crashing gas prices and clearance of past subsidy dues through the special banking arrangement have gone a long way in healing balance sheets and adding much needed green to the Profit and Loss statements.

Again, our company hasn't been an exception

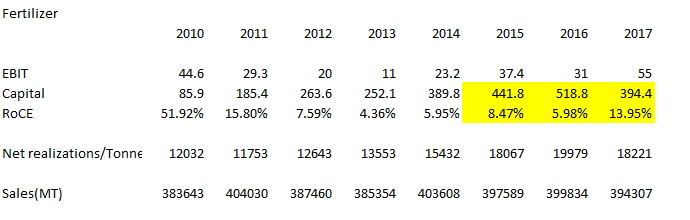

Since its coming to power, the NDA government has sworn to quicken the pace of subsidy clearances and reduce arrears through a special banking arrangement given to all fertilizer companies. With the implementation of the Urea Policy of 2015, companies have found it remunerative to produce at levels above reassessed capacity and this is exactly what the above graphic depicts. Pre 2015, even though the Kota plant operated at capacity levels north of 100% , increasing subsidy burden meant incremental capital burn with each passing year. This coupled with the non-remunerative and 'impractical' NPS-3 pricing formulae meant that Return on capital slid from the dizzy heights of 50% to low single digits by 2014. ( Side note : re-assessed capacity for DCMS stands at 379,000 TPA)

Post the implementation of the Urea Policy of 2015 which re-established the viability of excess production coupled with faster subsidy outgoes (subsidy outstanding at the end of FY'17 for the company has been pegged at 347cr v/ 451cr a year earlier) the business as a whole has become relatively less capital intensive and far more rewarding. This is evident from the near doubling of RocE's from 2014 to the end of FY'17 even though quantity sold has fallen.

Future Outlook - This space now looks much attractive as it hopes to get a series of fresh investments after a drought of 15 years as the central government plans to revive three sick fertilizer units and the possible entry of Jindal Steel into the sector. The implementation of the direct benefit transfer has hit a temporary snag but there seems to be a new found mojo among incumbents that the future will be relatively brighter than the rather inglorious past. With monsoons predicted to be at 98% of Long period average, there seems to be some head of steam building up at last.

The sugar cycle is fraught with its own share of dizzying uncertainty and timing it to perfection is a skill that resides in a select few. After ending the year in a surplus for six straight years between 2010 and 2016, global sugar stocks finally moved into deficit as India turned net importer of the commodity due to severe drought in the state of Maharashtra(home to 40% of the country's sugar production.) This coupled with the continuous diversion of sugarcane towards ethanol production in Brazil meant that there was a significant supply shortage which took prices on the ICE from lows of 10.5cents/lb in mid 2015 to recent highs of 22.5cents/lb.

The Indian sugar industry has long been at the mercy of both the central and state governments who have used the commodity as a popular means of populism among the rural population of the country. Sugar companies have perennially complained about the 'step-son' like treatment given to them at the behest of vote bank politics and the goverment's mandate of 'welfare of the poor.' Fixing of cane prices both at the central and state government levels dosent take into consideration the price of the final product - Sugar, as a result of which sugar mills, like fertilizer companies have been at the forefront of value destruction in the industry. The Rangarajan committee of 2014 alleviated a significant burden off the companies though there remains a lot more that needs to be done to completely take the shackles off the sector

DCM Shriram owns three sugar mills with a combined capacity of 33,000TCD and a co-generation facility which generates 94mw of power annually out of which 51mw is sold in the market. After reporting a De-growth in volumes of cane crushed between 2010-2016(2013 being an exception), FY'17 proved to be the turning year for the division volumes of cane crushed in the crushing season jumped from 282000MT in fy'16 to 412000 with an average recovery of ~11.1% . This led to sugar volumes jumping from 28.2 lac quintals in fy'16(with an average realization of 2638/quintal) to 36.6 lac quintals in fy'17(with an average realization of ~3530/quintal.)

Future Outlook - Sugar prices on ICE have nearly halved from the heights of 22.5cents/lb to settle in a range between 12.5-13 cents/lb currently. This hasn't had much of a ripple in domestic realizations though as top managements expect prices to remain stable. Tamil Nadu has witnessed its most severe drought in the past 100 years which means output from the 4th largest sugar producer from the country is likely to be tepid. On the other hand, Maharashtra is expected to bounce back with a 74'% increase in sugar production in the ensuing crushing season. International prices could stabilize around these levels going ahead as 13cents/lb is deemed to be the price at which more and more mills in Brazil divert their cane towards production of Ethanol. Another factor that could lend support to prices going ahead is that the US Department of Agriculture expects imports into India to increase in the coming year in-spite of higher production

|

| Snippet from the Q4 FY'17 Investor Presentation of DCM Shriram. Entry into the distillery segment would further DE-risk revenues from sugar price volatility |

|

| Snippet from the USDA Report |

Capital allocation remains the primary criterion when we judge management attitude towards the minority shareholder. DCM's management scores a high grade in this regard. Quick to smell the cash burn in the HKB Venture, the management has also reacted to the burgeoning working capital needs in the farm solutions business by downsizing its trading of complex fertilizers.

This is what the management had to say in the conference call for Q4 fy'17 -

We did the study of what has been the performance of our DAP/MOP trading business over the last –5-7 years and we found that with the fluctuation in the purchase prices, with certain fixation by government on the selling price and with the delayed subsidy coming from the government, the return on capital employed does not make business sense. So, we took a considered view evaluating our performance of the business over the last many years and then took a decision that it is better from the point of view our group’s financial health to stop doing this business

The farm solutions division remains a trading business by and large and any further scaling down on operations would only lead to increased delta in operating margins on the whole.

The chemicals business remains the bell-weather for the company by far. Within this division the company has a 1280TPD capacity(recently expanded from 780 tpd) of Chlor-Alkalis which it manufactures in the ratio of 1:0.88(meaning that for every 1mt of Caustic Soda manufactured, it gets 0.88tonnes of chlorine.) The Chlorine so obtained is then partly sold in open market and partly used in the manufacturing of PVC Resins. The PVC division is further integrated into polymer compounding and the Fenesta brand - which makes PVC frames for windows

Let me touch upon each product specifically -

Post its Q1 results for FY'17, Olin Corp - a global leader in Chlor-Alkalis has outlined a favorable view on Caustic Soda prices.

Future Outlook - The capital employed in this segment has more than doubled in the last 3 years due to the recent capacity expansion at Bharuch and the planned expansion at Kota for the coming year. As a result, RoCE's have halved - as the new capacities come on stream and get fully absorbed. Management expects the recently upgraded Bharuch to contribute meaningfully for the full year thereby propelling capital efficiency and in turn driving RoCE's. (side note - current capacity utilization stands at 77% , management expects this to cross 80 comfortably in the future. The management has upgraded the Bharuch facility with the membrane cell technology which further aids power efficiency. It plans to do the same in the Kota plant in the coming year)

The Indian PVC Resin market stands currently at around 3-3.5 Million tonnes/annum. At current prices of 75-77/kg the industry size is pegged in the region of 22,500 to 25,000 crores. DCMS has a 70,000 tonne capacity and runs at utilization north of 90% . With no capex planned as of now this unit becomes the cash cow within the chemical division as the working capital cycle in this business is miniscule which helps management to generate sufficient free cash to fund its overall operations

Among the smaller businesses, Bioseeds has been a volatile business for the company courtesy the overseas operations in Philipines and Vietnam and price regulations on Bt cotton seeds domestically. DCMS has taken a one time hit of 85cr in Bioseed's international operations owing to 'high gestation periods and large losses.' The domestic operations are set to pick up steam as farmers shift from sowing pulses(due to their UN-remunerative MSP's) to cotton.

|

| (Courtesy - Financial express) |

Finally, the Fenesta brand of UPVC Windows that was established as a forward integration of the PVC Resins manufactured in house seems to be growing at a healthy notch. According to the investor presentation for FY'17, the segment revenues stand at 283cr registering a growth of 20% YoY and the order book stands at 430cr , providing a revenue visibility for the next 18 months or so. Management claims that operations are PBT Positive however hasnt backed it up with financial data.

Any analysis isn't complete without a hygiene check of the books. We examined all the available subsidiaries of DCMS and found a couple of striking points

DCM Shriram Infrastructure is a step down subsidiary of DCM Shriram Investments and Finance which in turn is a subsidiary of DCMS(the parent.) What we found was that DCMS has invested a sum of 30cr approx in this entity through an inter-corporate deposit. This money has been invested in some sort of fixed asset addition which seems to be stuck in the CWIP phase. As per available data between 2014 and 2016, this has remained status quo without any further information since.

Another noteworthy point is a 95cr loan in Shriram Bioseed ventures given by the parent. This presumably forms part of the 85cr hit that DCMS standalone has taken on its books this year as impairment in the overseas operations of Bioseed

|

| Notice the deployment of the long term borrowings into the mysterious CWIP |

Daniel James Brown, in his book "The boys in the boat" narrates an anecdote of how nine working class men from Seattle won gold at the 1936 for Rowing. Reflecting on the effort it took to be part of world-class crew team, he quotes the boat-builder George Yeoman Pocock:

“It is hard to make that boat go as fast as you want to. The enemy, of course, is resistance of the water, as you have to displace the amount of water equal to the weight of the men and equipment, but that very water is what supports you and that very enemy is your friend."

After tiding through stormy waters, DCMS seems to be gearing itself up for sustained business momentum in coming times. Perseverance is a difficult task to master as companies and managements fold up right when the fruit of prosperity ripens. The Shriram brothers have done just enough to tide through the despair, will they now cherish the exuberance?

On the backdrop of the above set of information gathered from available sources, we will now dig further into the company's quantitative metrics and post our follow-up in due course

Disclaimer : We have no vested interest in the stock discussed above and this is not a recommendation in any way. Do your own research before making any investment decision

Hi,

ReplyDeleteWhat do you feel about Sinclair Hotels.

Hi,

ReplyDeleteWe would not want to discuss about stocks we dont cover or have no insight on. Thanks.

Excellent analysis..... Thanks

ReplyDelete