In

our previous post on the Indian sugar sector, we discussed how

incumbents have found it extremely difficult to operate in a myriad of

regulations that govern the operating cycle of the industry.

In

this post we have tried to present a picture of how the companies in

the sector stack up against each other by comparing them across some

parameters that we find useful in comparing companies in the sugar

sector and have highlighted our findings below:

Commodity

businesses derive their moats from being cost leaders and generally industry

leaders tend to be the

most efficient companies in the business as economies of scale works to their

advantage. The cost intensity of manufacturing sugar means that companies must

optimize cane procurement and conversion processes so as to increase the

recovery rate.

However, as we can see in the sugar sector the leader seems to be reeling under extreme stress. We already know that a leveraged balance sheet in a cyclical sector lends itself to a plethora of pain when the force of gravity imposes itself on the business. The manufacturing of sugar is both fixed and working capital intensive and only a select few are able to withstand the wild cyclical swings. Shishir Bajaj led Bajaj Hindustan is the industry leader with a crushing capacity of 136,000TCD and has been the torch bearer of the stress faced by companies across cycles

However, as we can see in the sugar sector the leader seems to be reeling under extreme stress. We already know that a leveraged balance sheet in a cyclical sector lends itself to a plethora of pain when the force of gravity imposes itself on the business. The manufacturing of sugar is both fixed and working capital intensive and only a select few are able to withstand the wild cyclical swings. Shishir Bajaj led Bajaj Hindustan is the industry leader with a crushing capacity of 136,000TCD and has been the torch bearer of the stress faced by companies across cycles

We

have compared Bajaj Hindustan to Balrampur Chini and Dwarikesh Sugar on

select

parameters to understand why the sector leader has performed in this

fashion and how other companies have taken advantage of this and have highlighted our findings below -

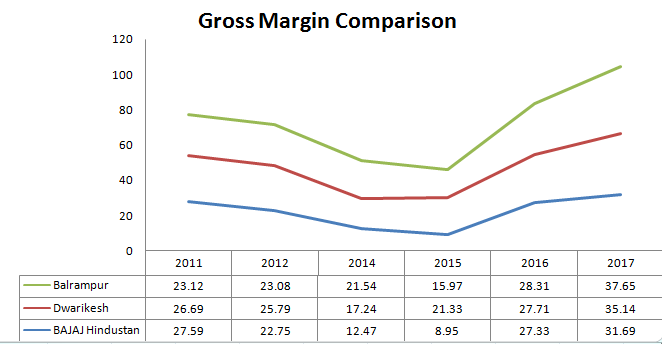

- We first compared the gross margins of these companies to understand profitability that accrues to the sector. Incremental gross margins for an integrated sugar company are primarily driven by the sale of associated by-products as the marginal revenue accruing from these is significantly higher than the marginal cost incurred in the conversion process

The observations from the above data

are quite intriguing especially in light of the fact that Bajaj Hindustan actually has the lowest contribution from sugar to

its overall revenues

Sugar contribution to overall revenues for the three

companies

|

- The most common yardstick of a mill's efficiency is the recovery rate of sugar. Within Uttar Pradesh, mills located in the eastern region of Bijnor have the highest recovery rates, due to usage of high-yielding early sugarcane varieties like CO 0238. These early varieties of sugarcane fetch the farmer Rs 10 more per quintal than the general variants.

Bajaj Hindustan's mills are predominantly situated in and around the district of Lakhimpur Kheri which is towards the southern part of the state. We took the recovery rates for both DCM Shriram (a listed peer with a presence in the same region) and Bajaj to check how recovery rates differ for both companies

The

difference in recovery rates is quite stark and as both companies have mills

around similar geographies. To understand why Bajaj Hindustan has sub-optimal

gross margins and recovery rates, we compare

and analyze the cash conversion cycle for BHSL vis a vis its peers

The

payable days for Bajaj Hindustan are nearly four times its peers - thereby

leading to higher COGS as the company is obliged to compensate in the form of

interest payments on its dues to farmers. Sugar companies have to keep

a high inventory component as crushing is a seasonal activity but demand for

sugar is secular, and while the other companies finance this through working

capital loans, BHSL does it through delaying cane payments as the balance sheet

does not have scope for further leverage

Keeping

the cane farmer happy is central to the sustainability of this business - and

any delay in payments has a prolonged impact on the goodwill of a sugar mill.

Add to that, the penal consequences imposed on delayed disbursements are severe

as the state government has imposed strict norms to ensure timely payments.

|

| Source: Financial Express, 13th April 2017 |

The

natural chain of events would suggest to us that Bajaj Hindustan would

invariably face the wrath of the farming community in the form of both

low quality as well as quantity of supplies. We took the crushing

capacity / day for Dhampur Sugar and Dwarikesh Sugar (both of whom have a

presence in the area of Bijnor) in our effort to understand the root

causes of in-efficiency for BHSL

| |||

| (Bajaj Hindustan and Dwarikesh both changed their accounting months in 2014 and 2015 respectively) |

Despite having the largest capacity, Bajaj Hindustan operates its mills for the least number of days in comparison to peers. The underlying scale of business hence loses out to operational in-efficiency, thereby creating a lollapalooza of ever surmounting debt and farmer agitation thus leaving the company in a situation of mess which is difficult to come out from.

We will continue this post with further work on companies highlighting how they have positioned themselves differently so that once this honeymoon period for sugar sector gets over how can they emerge better positioned to weather the downturn in cycle that awaits them in future.