How it used to be in the earlier days...

Back in the twentieth century, the market for chemical based photographic processes was dominated by a single player. The industry hadn't changed much in over a hundred years and any in-roads that amateurs made was through their distribution and not innovation. Either ways, taking on Eastman Kodak wasn't an easy task by any mean.

Back in the twentieth century, the market for chemical based photographic processes was dominated by a single player. The industry hadn't changed much in over a hundred years and any in-roads that amateurs made was through their distribution and not innovation. Either ways, taking on Eastman Kodak wasn't an easy task by any mean.

and then, what innovation did..

The oil embargo and soaring inflation of the seventies led to an astronomical rise in silver prices - a key ingredient in the film processing industry. Incumbents such as Eastman and Fujifilm found business incredibly hard to come by , though this ultimately proved to be a mere passing shower rather than a full fledged storm. However in the midst of all of the turbulence, Minoru Ohnishi - the then CEO of Fuji Photo was already preparing for a tsunami of change that the industry was about to witness. In 1984. Sony launched its path breaking digital camera - Mavica. In the ensuing 15 years, Fuji spent nearly $ 2bn in R&D to ramp up on digital photography. The result? Fuji gained almost all of the incremental market share in digital picture processing - it had 5,000 labs across the globe. Eastman Kodak was now where Fuji was twenty years back - it could muster up a mere 100 labs

The above illustration has been plucked from Rita Gunter McGrath's book on competitive advantage. The basic premise that the book has been written on is that competitive advantages for any company cannot sustain over long periods of time. Even though I would not totally agree on that premise, however, in the context of this post we will use it as a reference point. Take for instance the case of RIM - the company that manufactures the now obsolete Blackberry handsets. Blackberry had become the choice of the masses - from businessmen to savvy youngsters, everyone wanted a piece of the glam. Today, the company fights for its mere existence. The cause for decline? Complacency.

How status quo is changing...

A thought provoking idea for any investor/entrepreneur stems from the fact of defining the word 'competition.' Consensus believes that competition comes from rivals selling similar products within the same industry. However, companies today face competition from within the same industry as well as from external forces that threaten to substitute the very validity of existing business models. Sandeep Engineer(the promoter of Astral Poly) in one of his speeches alluded to how he pushed the use of C-PVC pipes as an alternative to traditionally used Galvanized Iron pipes in industries - a classic example of one business model fighting it out against the other. Till then, plastic pipes were an anomaly, today it's the order of the day. This serves us an example of how business models can change and the earlier indications are slow, unnoticeable. However, complacency is the breeding ground for competition to take over and snatch what earlier was yours. Companies & Industries that have understood this have flourished, while those who didn't have rightly become extinct.

What competition is doing today and how to survive...

In today's world, disruption is the catch phrase of the masses. So much so that savvy investors and entrepreneurs live by it. Consensus believes that incumbents across business lines will find it increasingly difficult to cope up with the pace of disruption and legacy business models are no longer tailor made to sustain longsighted growth as seen in the past. Today, you'd find most stories on how businesses are driving themselves to extinction like Kodak did because management teams have failed to deploy capital productively in an environment of transient advantages.

Professor McGrath in her book shares her observations regarding certain companies who have successfully navigated disruptions in their businesses to emerge with stronger and more durable moats. She states that one of the patterns to look for in organizations that have mastered transient advantage environments is the way they continuously free up resources from old legacy advantages in order to fund the development of future ones - with the one goal of earning higher/stable returns on incremental capital employed. In simple words, they abhor status quo, creating an organization, agile enough to adapt. This in turn leads to longevity.

In the light of the above points, I would like to discuss about a company that bears an uncanny resemblance to the points mentioned above:

-being a leader in an ageing business,

-generating significant cash flows

-re-deploying those cash flows into businesses earning higher incremental returns on capital employed.

SRF Limited:

One of the hallmarks of a good management team is that they are masters of disengagement - "the process of moving out of an exhausted opportunity". This is as core to their skill set as is innovation, growth and exploitation of new business avenues. These management teams continuously evaluate business areas and any early warning signs are paid heed to, rather than ignored.

Being a market leader in an ageing industry is a daunting proposition for any management team. Over the years, the market for Nylon Cord Fabric (a key component used in the making of a bias ply tire) has matured to the point of stagnation. Incremental returns have consistently moved lower owing to the widespread shift to radials across the globe.

SRF, the world's second largest maker of the fabric has been no exception to this change. However, let's see what Arun Bharat Ram (Chairman of SRF) has to say in one of his annual letters to shareholders-

|

| Disengagement |

Sale of Nylon tire fabrics has traditionally formed the backbone of the technical textiles division in particular and the company at large. In the face of a declining market for its product, the management consciously took a decision to scale down the business to focus on the chemicals and polyester business.

I'll touch upon each of these segments individually:

|

| Notice how Revenue contribution of technical textiles has halved over the years |

The bedrock of the chemicals division of the company lies in the application of fluorine for both refrigerant gases and specialty chemicals. The fluorine molecule is one of the most hazardous elements known to man and its handling and application is a highly critical process as it is one of the most chemically reactive elements.

Refrigerant gases are a key component used in cooling devices such as refrigirators and Air-conditioners. SRF is the sole supplier of HFC-134a in India and is the undisputed market leader with a market share of around 50 percent.

This is what the management had to say in one of the concalls

After establishing itself in the domestic market (annual demand 8,000 tonnes, growing at 12-15%) , SRF has now targeted the American market which imports around 30% of its annual requirement of 110,000 tonnes. Chinese imports of these gases are now subject to an anti dumping duty and SRF is well poised to make deep inroads into the country. The first steps have already been taken as orders from Walmart are witnessing strong traction with time. An 8000 tonnes opportunity in India with a 50 percent market share versus a 33000 tonnes opportunity in the USA tells you that they have barely scratched the surface in this segment.

Specialty Chemicals on the other hand is a R&D driven business wherein the technology to produce a certain set of requirements of global agro chemical and pharmaceutical giants lies solely with the company. Around 80% of revenues come from agro-speciality and the rest from pharma-speciality. SRF over the years has filed for 94 proccess patents and has developed a strong IPR base which enables the company to successfully scale up products that are inherently complex to produce on a large scale.

The company has currently commercialized around 60 molecules and is in the process of developing around 40-50 more through dedicated plants for each molecule (each dedicated plant entails a capex of around 50 to 70cr)

| This business enjoys high customer stickiness due to the critical nature of the product |

SRF's packaging division focuses on BOPET and BOPP films that are manufactured in its plants in India and South Africa. This is what Mr Ram has to say about the business in his latest annual letter

Testing management credibility is an important part of the work we do on companies.

Firstly, we took financial data of the past 10 years for SRF's packaging division and its competitiors - Cosmo Films and Jindal Poly to ratify their repeated claims of being the lowest cost producer. The excel sheet is attached below:

The numbers show two things -

one, the hugely volatile nature of the industry,

two, the margins have been much more consistent and linear for SRF versus competitors over last few years.

One of the technical factors for the above that the management alluded to in a analyst call is that most of the films manufactured are below 12 microns in thickness and are chemically coated. Competitive pressures are relatively lower in this segment as most of the domestic and Chinese capacity manufacture films that are thicker than 12 microns and may/may not be coated.

Secondly.....

The art of creating value for stakeholders is a function of how well one allocates capital. Warren Buffet, in his 1987 letter states that a corollary of efficient capital allocation is that there comes a time when shrinking businesses and extinguishing capital through buybacks is a wiser choice than expanding through acquisitions or capital expenditures. Back in 1997, the domestic NTCF industry was highly fragmented. Companies who made tires had 'backward integration' to make Nylon fabrics as well - a classic case of capital burn because there was no shortage of fabric in the market.

SRF which was then a Rs 283 crore conglomerate acquired CEAT's plant for Rs 325 crores. Ambitious, you might say? Lets look at the demand supply scenario in the domestic market for the next 5 years

|

| (Source - SRF 2001 Annual Report) |

|

| The strong player |

Post all the inorganic expansions that were implemented, SRF moved from being the 8th largest NTCF maker in the world to becoming the 2nd largest globally. It has since maintained its position, thereby generating huge amounts of free cash as the business does not require incremental capital to grow(classical Warren Buffett business).

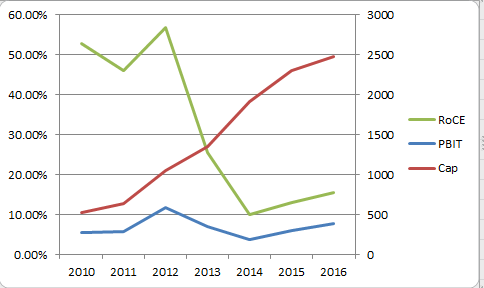

|

| Capital employed and RoCE of technical textiles |

So what did SRF do with so much free cash? Lets find out...

|

| Capital employed across all three divisions - Notice how management has built the chemical and packaging business |

“As we announced earlier, we have a plan to invest around INR3,500 crore in the next four years and around 70% of the investments are earmarked for the Chemicals business. Therefore, I would reiterate here, that the chemical space remains a key segment for the Company and our strategic intent to further grow the business remains intact.”

|

| Chemicals RoCE |

A closer look at the RoCE graph of the chemicals business reveals that though the management has continuously pumped in incremental growth capital, the RoCE's have fallen from high 50's to 15% as of FY'16 - this is primarily down to the fact that the windfall from carbon credits for the company(which cumulatively amounted to more than Rs 10bn) stopped from FY'14 onwards, thus normalizing returns.

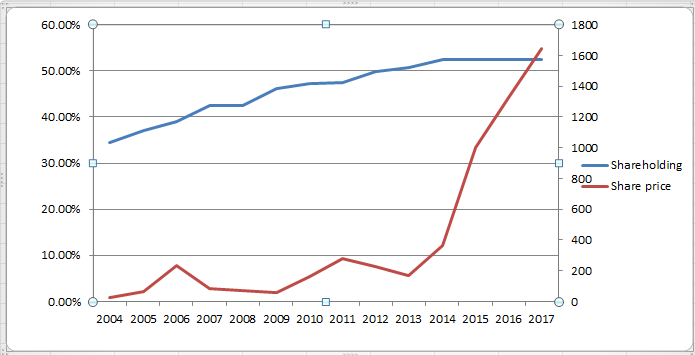

Lastly, we checked for - their skin in the game - we compiled data for the past 13 years to see the change in promoter shareholding. The excel is attached below

|

| SRF's promoters have increased their stake from 34% in 2004 to 52% in 2017 |

As the moat that protects the castle dries up, it needs to be refurbished so as to protect the kingdom. The management team led by the Ram family have successfully managed to transform SRF's business from being an ageing textile manufacturer to a lean, dynamic and technoogy driven chemical conglomerate.

Ill end by quoting the famous Ben Franklin.

"When you're finished changing, you're finished."